Quantopian Long Trading Model

includes: Chart, Code

Summary

The model finds small cap equities that have dropped at least 8% during the previous trading day and holds them for 5 days. The trading model beats the S&P 500 during some periods of time and can be used when its relative performance has been poor. It would not be effective if the strategy was implemented in all market environments.

Strategy

-

Security Selection. The trading model creates a pipeline of equities based on fundamental factors such as market capitalization. Securities must have market capitalizations that are less than $1 billion and greater than $500 million. The pipeline also screens for securities that are actually tradeable to investors.

-

Portfolio Leverage. The model uses up to 30% leverage. If the maximum portfolio leverage is reached, the model does not make additional purchases.

-

Fill Prices. Price slippage is accounted for on the Quantopian platform. Because limit prices are used, if an order is not able to be filled by the end of the day, it is canceled.

-

Orders. If the security fell more than 8% in the previous trading day, a limit order is placed for that security at the previous day’s closing price. An allocation of 13% of the portfolio is made and the position is completely closed after the 5 day period.

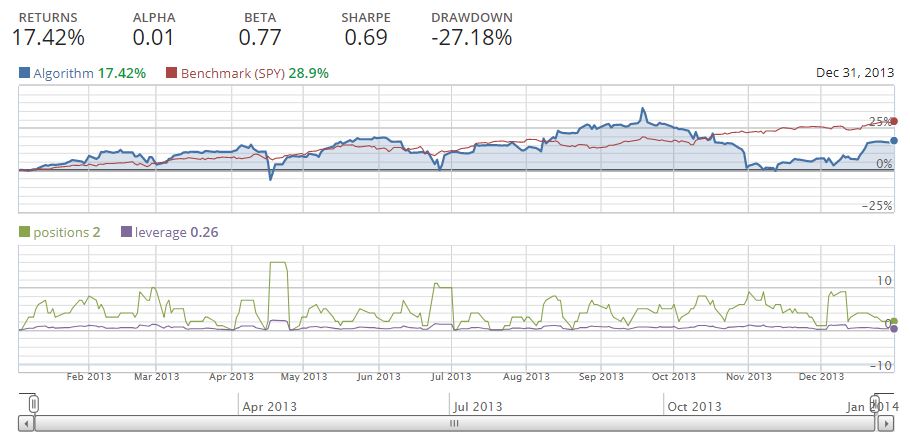

Performance

During a one year period, the trading model returned 17% versus 29% for the S&P 500. Overall the model does not perform better than the benchmark on a consistent basis.

Model Implementation

This model would be useful when its relative performance to the benchmark S&P 500 has been poor. During these times, investors have an opportunity to beat the benchmark as the model “catches up” in relative terms. Investors would not benefit from using the trading model consistently over time as it does not match benchmark returns and also has large drawdowns in portfolio values.

Here’s the beginning of the chart indicating performance:

from quantopian.algorithm import attach_pipeline, pipeline_output

from quantopian.pipeline import Pipeline, CustomFactor

from quantopian.pipeline.data.builtin import USEquityPricing

from quantopian.pipeline.factors import SimpleMovingAverage, RSI, AverageDollarVolume

from quantopian.pipeline.data import Fundamentals

from quantopian.pipeline.filters import QTradableStocksUS

import talib

import numpy as np

import pandas as pd

from quantopian.pipeline import factors, filters, classifiers

from quantopian.pipeline.classifiers.fundamentals import Sector

import quantopian.algorithm as algo

def initialize(context):

set_commission(commission.PerTrade(cost=1))

context.maxlv = 1.3

context.days_elapsed = {}

context.can = []

# Create and attach an empty Pipeline.

pipe = Pipeline()

pipe = attach_pipeline(pipe, name='my_pipeline')

context.cannot = []

context.rsis = {}

context.buys = []

# Available technical analysis factors ------------------------------------------

# sma_10 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=10)

# sma_30 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=30)

# sma_1 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=1)

# sma_50 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=50)

# sma_200 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=200)

# dollar_volume = AverageDollarVolume(window_length=30)

# Filter construction

# previous greater than limit = 200000000000

# sma_greater = sma_50 > sma_200

# prices_under_5 = (sma_10 < 20)

big_market_cap = Fundamentals.market_cap.latest < 10000000000

tradable_stocks = QTradableStocksUS()

# can put this in - tech_sec = Sector().element_of( [311])

low_market_cap = Fundamentals.market_cap.latest > 500000000

# volume = dollar_volume > 100000

# fundamentals.asset_classification.morningstar_sector_code == 301)

# Register outputs.

# pipe.add(sma_10, 'sma_10')

# pipe.add(sma_30, 'sma_30')

# pipe.add(sma_1, 'price')

pipe.set_screen(big_market_cap & tradable_stocks & low_market_cap)

schedule_function(current_positions,date_rules.every_day(), time_rules.market_close())

schedule_function(buy_sell_orders,date_rules.every_day(), time_rules.market_open(minutes=1))

schedule_function(empty_can,date_rules.every_day(), time_rules.market_open(minutes=25))

def empty_can(context, data):

context.can = []

def before_trading_start(context, data):

results = pipeline_output('my_pipeline')

# Store pipeline results for use by the rest of the algorithm.

context.pipeline_results = results

context.security_list = context.pipeline_results.index

context.pos_for_day = 0

if context.account.leverage < 1.1:

for security in context.security_list:

hist = data.history(security, 'price', 14, '1d')

price_2 = hist[-2]

price_1 = hist[-1]

price_dif = (price_1-price_2)/price_2

if -.12 < price_dif < -.06 and 1 < price_1 < 6 and security not in context.cannot:

context.can.append(security)

# print(security, round(price_1,2), round(price_dif,2))

# print('Can:', context.can)

for stock in context.days_elapsed:

context.days_elapsed[stock] += 1

record(leverage = context.account.leverage)

record(positions = len(context.portfolio.positions))

def buy_sell_orders(context, data):

# results = pipeline_output('my_pipeline')

# # print results.price

for security in context.can:

hist = data.history(security, 'price', 2, '1d')

price_1 = hist[-1]

if (

security not in context.portfolio.positions

and context.account.leverage < context.maxlv

# and len(context.can) < 50

and context.pos_for_day < 15):

hist = data.history(security, 'price', 20, '1d')

# print(hist)

rsi = round(talib.RSI(hist, timeperiod=14)[-1],0)

if security not in context.rsis:

context.rsis[security] = rsi

# print('rsi_list', context.rsis)

# print('sec:',security,'rsi',round(rsi,2))

order_percent(security, .13, style=LimitOrder(price_1))

context.days_elapsed[security] = 0

context.pos_for_day += 1

# print("Bot:", security, context.maxlv, round(context.account.leverage,3))

if len(context.portfolio.positions) > 0:

for security in context.portfolio.positions:

# print('sma', round(sma_10,2))

if context.days_elapsed[security] > 5:

# print(security, sma_10, 'sell - 10')

# print(security, sma_30, 'sell-30')

order_target(security, 0)

# print("sold:", security)

def current_positions(context, data):

if len(context.portfolio.positions) > 0:

# Avaialable RSI Factor (for price performance comparison)

# for security in context.portfolio.positions:

# prices = data.history(context.stocks, 'price', 20, '1d')

# hist = data.history(security, 'price', 20, '1d')

# print(hist)

# rsi = talib.RSI(hist, timeperiod=14)[-1]

# # print(rsi)

# context.rsis.append(rsi)

# avg_rsi = round(np.average(context.rsis),2)

# record(RSI = avg_rsi)

# print('average', avg_rsi)

all_positions = "Current positions for %s : " % (str(get_datetime()))

for pos in context.portfolio.positions:

if context.portfolio.positions[pos].amount != 0:

all_positions += "%s -- %s shares, %s days, " % (pos.symbol,

context.portfolio.positions[pos].amount,

context.days_elapsed[pos])

log.info(all_positions)